Have you ever wondered how accounting originated? And who invented this science? And how were the transactions of people before the birth of the accounting science? And what stages did this science go through until we reached the accounting science that we know today?

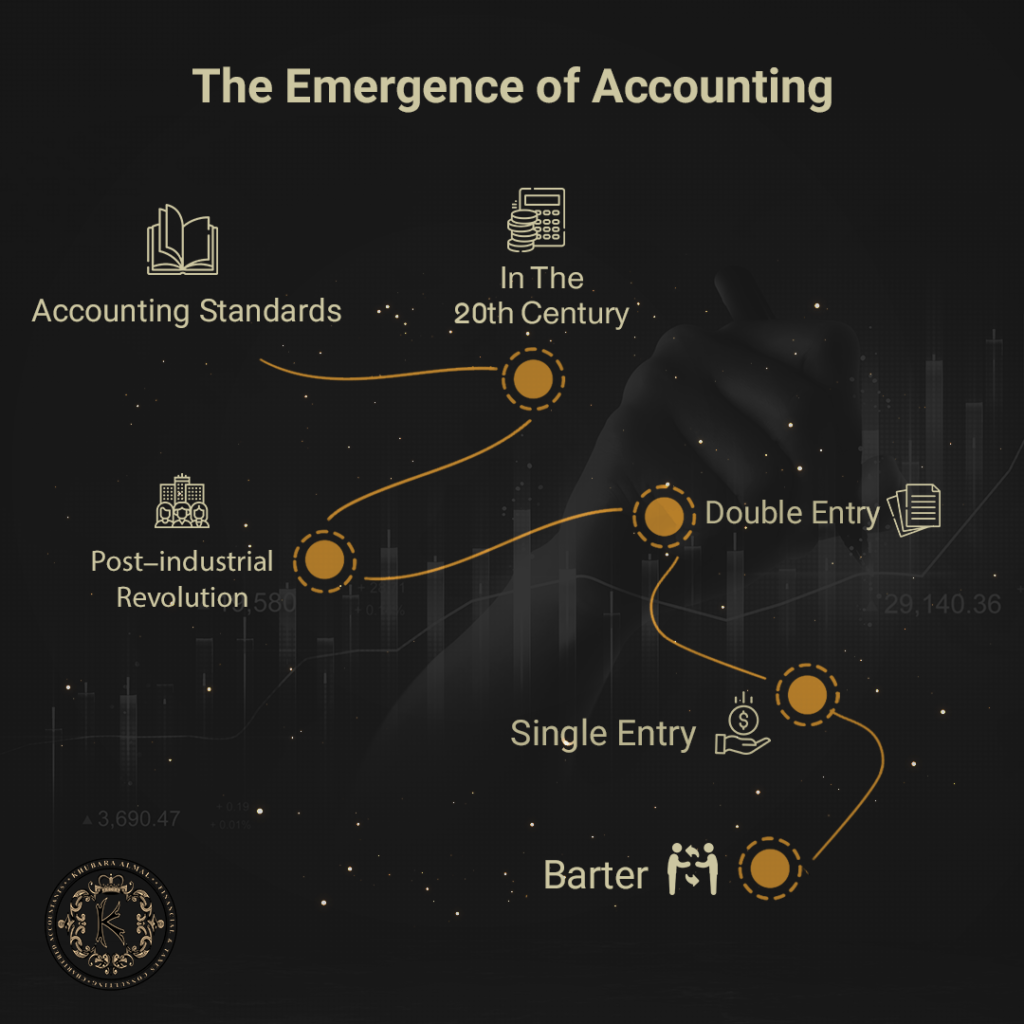

To answer these questions, we need to go back in time around 3000 BC. At the time, humans were using the barter system to conduct commerce. They were exchanging tools, food, weapons, minerals, etc. in a way that satisfies both sides of the exchange process. However, it soon became difficult to continue with the barter system due to the unevenness of this process. Then, to facilitate transactions among people, the need for fixed money appeared. Perhaps the king of Lydia (Aliatus) was the first to mint the first official currency in the world. It was a mixture of gold and silver and from here the journey of money in the world began.

With the emergence of paper money, which appeared in China 770 BC, there was a need for a science that organizes and summarizes all financial transactions, that was the accounting science. Hence, we understand that accounting is one of the ancient sciences that appeared in many ancient civilizations such as the Egyptian, Romanian, Chinese, Babylonian, and Greek civilizations. It was called “The Science of Accounting”, and it was concerned with recording imports and expenses in an account statement that shows how to benefit from these resources.

After that, accounting started to develop until it reached its current form through three stages. These three stages are as follows:

1- Single entry stage:

This stage appeared in conjunction with the beginning of the use of money in commercial transactions as an alternative to barter in the Middle Ages until the year 1494. This stage was intended to record the financial operations in books to be used later in extracting the results of the movement of funds—whether gains or losses—in a specific period of time. At that time, there was only financial accounting.

2- Double Entry Stage:

In this stage, credit is due to the Italian mathematician LUCA PACIOLI who gave a detailed description of the double-entry rule which formed the basis for bookkeeping since 1494.

The most important features of this phase are:

– The issuance of overland trade law that was called “Savary Law” by the French jurist (Jacques Savary) in 1673.

– The issuance of a maritime commercial law for the year 1681.

– The emergence of cost accounting.

3- Post-industrial revolution stage:

This stage began in 1776 due to the industrial revolution, which led to the formation of joint stock companies to invest huge capital in industry. This stage also showed the actual significance of cost accounting.

The twentieth century has been marked by the increased number of projects, the merger of companies phenomenon, the great progress in inventions and technology, and the entry of foreign investments. Thus, accounting developed more and more not only to become a mean to measure the efficiency of the administration, but also to serve the whole society on a larger scale.

Then, accounting branched out into multiple fields, and each branch serves a specific field to serve the administration on the one hand and measure its efficiency on the other hand.